What Is a QDRO, and Why It Matters in an Illinois Divorce?

Divorce isn’t just about dividing property today, it’s about protecting your financial future. One of the most overlooked (and most important) documents in an Illinois divorce involving retirement accounts is a QDRO, or Qualified Domestic Relations Order.

If a retirement account is divided incorrectly, or not divided at all, the consequences can be costly, permanent, and hard to fix later. Below is what you need to know, and why having the right legal help matters.

What Is a QDRO?

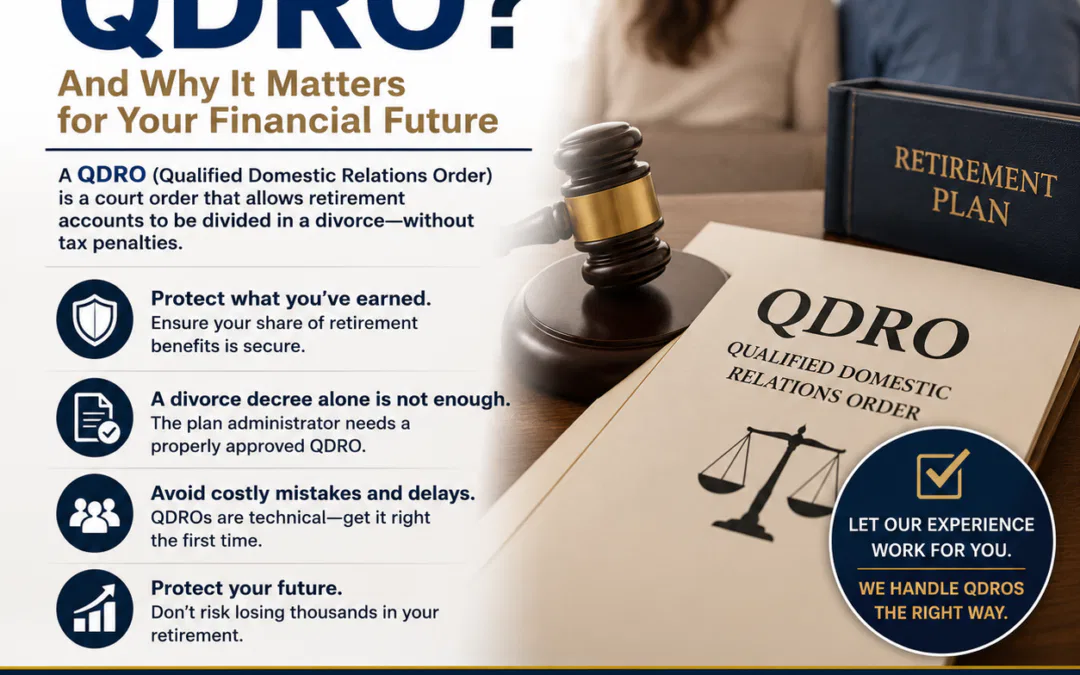

A Qualified Domestic Relations Order (QDRO) is a court order that allows retirement benefits to be divided between spouses during a divorce without triggering taxes or early withdrawal penalties.

In simple terms, a QDRO tells the retirement plan administrator:

- Who gets a share of the retirement account

- How much they receive

- When and how those funds will be paid

Without a properly drafted and approved QDRO, the retirement plan will not divide the account, even if your divorce judgment says it should.

What Types of Accounts Require a QDRO?

QDROs are commonly required for:

- 401(k) plans

- Pensions

- Profit-sharing plans

- Other employer-sponsored retirement plans

IRAs generally do not require a QDRO, but they still must be divided carefully to avoid tax consequences.

Why a Divorce Judgment Alone Is Not Enough

This is where many people run into trouble.

Even if your divorce decree clearly states that a retirement account is being divided, the plan administrator will ignore it unless a valid QDRO is entered and approved.

That means:

- The account stays in one spouse’s name

- The other spouse has no direct right to the funds

- If the account holder retires, withdraws funds, or passes away, benefits can be lost

Once time passes, fixing these mistakes can be difficult, or impossible.

Why QDROs Are So Easy to Get Wrong

QDROs are technical legal documents governed by:

- Federal law (ERISA)

- Plan-specific rules

- Illinois family law requirements

Common problems we see include:

- Using generic or online QDRO templates

- Incorrect valuation dates

- Failing to address survivor benefits

- Language rejected by the plan administrator

- Divorce cases closing without a QDRO ever being entered

These errors can delay distribution, cause denial by the plan, or result in unexpected taxes.

Why You Should Have a Lawyer Handle Your QDRO

A QDRO is not just paperwork, it is a legal order that directly affects your retirement security.

When you work with the Law Office of Jonathan W. Cole P.C., we:

- Coordinate the QDRO with your divorce judgment

- Draft plan-specific language that meets administrator requirements

- Communicate with retirement plan administrators

- Ensure the order is properly approved and entered by the court

- Protect your rights before the divorce is finalized

Most importantly, we make sure your retirement division is done correctly the first time.

Why Timing Matters

QDROs should be prepared as part of the divorce process, not years later. Waiting can create serious risks:

- Account balances change

- Employers change plans

- Participants retire or pass away

- Benefits are paid to the wrong person

Addressing the QDRO promptly helps prevent future disputes and protects both parties.

Final Thoughts

If your divorce involves a retirement account, a QDRO is not optional, it is essential. A properly prepared QDRO ensures that what was agreed to in your divorce is actually enforced, without unnecessary taxes, penalties, or delays.

Cutting corners now can cost you years of retirement security later.

📞 If you are going through a divorce or need help with a QDRO, contact the Law Office of Jonathan W. Cole P.C. at (708) 529-7794 — Your Neighborhood Law Firm.