How a Credit Shelter Trust Works, And When You Should Consider One?

Estate planning is about more than just deciding who inherits your assets. For many families, it is also about protecting wealth, minimizing estate taxes, and ensuring long-term financial security for a surviving spouse and children. One planning tool that can help accomplish those goals is a credit shelter trust, sometimes called a bypass trust or family trust.

While changes in federal estate tax laws have reduced the number of people who need this type of trust, it can still be a powerful option in the right circumstances. Understanding how it works, and when it makes sense, is key.

What Is a Credit Shelter Trust?

A credit shelter trust is an estate-planning trust typically created by married couples. It is designed to take advantage of the federal estate tax exemption available to each spouse.

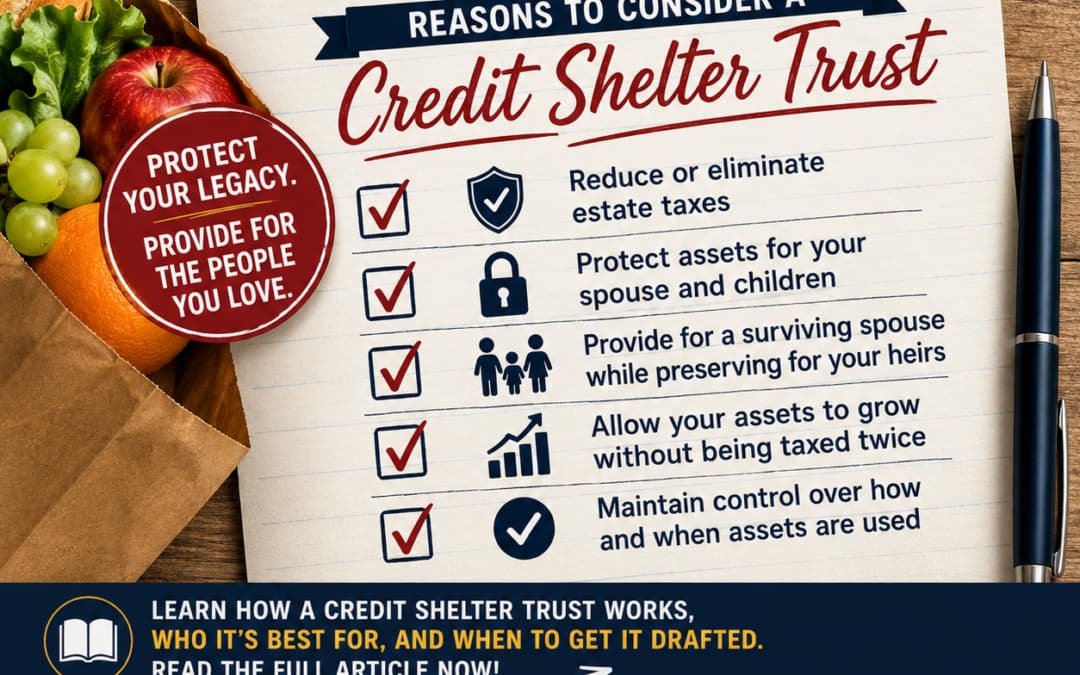

When the first spouse dies, a portion of their estate (up to the available estate tax exemption) is placed into the credit shelter trust instead of passing outright to the surviving spouse. Those assets are then “sheltered” from estate tax, both at the first death and when the surviving spouse later passes away.

The surviving spouse can usually:

- Receive income from the trust

- Access trust principal for health, education, maintenance, and support

- Continue living in a home held by the trust

However, the trust assets are not counted as part of the surviving spouse’s taxable estate, even if they grow significantly in value.

How a Credit Shelter Trust Works in Practice

Here’s a simplified example:

- A married couple has a combined estate of $12 million.

- One spouse dies, leaving $6 million in assets.

- Instead of leaving everything outright to the surviving spouse, $6 million is placed into a credit shelter trust.

That $6 million:

- Uses the deceased spouse’s estate tax exemption

- Is removed from the surviving spouse’s taxable estate

- Can grow tax-free from an estate tax perspective

When the surviving spouse later dies, only their own remaining assets are subject to estate tax, not the assets held in the credit shelter trust.

Who Is a Credit Shelter Trust Best For?

A credit shelter trust is not necessary for everyone, but it can be especially useful for:

1. Married Couples With Larger Estates

Couples whose combined assets approach or exceed the federal estate tax exemption may benefit from locking in each spouse’s exemption through a trust structure.

2. Families Concerned About Future Estate Tax Changes

The federal estate tax exemption is not permanent. It has changed many times and is scheduled to decrease in the future unless Congress acts. A credit shelter trust can help protect against future reductions.

3. Second Marriages or Blended Families

A credit shelter trust allows a spouse to provide for a surviving spouse during their lifetime while ensuring that remaining assets ultimately pass to children from a prior relationship.

4. Asset Protection and Control Goals

Because the trust owns the assets, it can provide:

- Protection from creditors

- Protection from remarriage risks

- Long-term control over how and when assets pass to children.

When Should You Have a Credit Shelter Trust Drafted?

A credit shelter trust should be considered during the estate-planning process, not after a spouse has passed away. Once the first spouse dies without the trust in place, the opportunity to use this strategy may be lost.

You should strongly consider discussing a credit shelter trust if:

- You are married and have accumulated significant assets

- You expect asset values to increase over time

- You want to preserve wealth for children or grandchildren

- You are concerned about future changes in estate tax laws

Even if a credit shelter trust is not ultimately needed, reviewing the option ensures your plan is flexible and future-proof.

Is a Credit Shelter Trust Still Relevant Today?

Because federal estate tax exemptions are currently high, many families no longer need credit shelter trusts strictly for tax reasons. However, estate planning is not static. Laws change, asset values grow, and family situations evolve.

For some families, a credit shelter trust remains a valuable tool, not only for tax planning, but also for control, protection, and peace of mind.

Talk to an Illinois Estate Planning Attorney

Every family’s situation is different. The right estate plan depends on your assets, your family structure, and your long-term goals.

If you are wondering whether a credit shelter trust makes sense for you, or if you want to review an existing estate plan, the Law Office of Jonathan W. Cole P.C. can help.

📞 Call (708) 529-7794 to schedule a consultation and make sure your estate plan is built to protect the people and legacy that matter most.

Your Neighborhood Law Firm.